The information provided on this publication is for general informational purposes only. While we strive to keep the information up to date, we make no representations or warranties of any kind about the completeness, accuracy, reliability, or suitability for your business, of the information provided or the views expressed herein. For specific advice applicable to your business, please contact a professional.

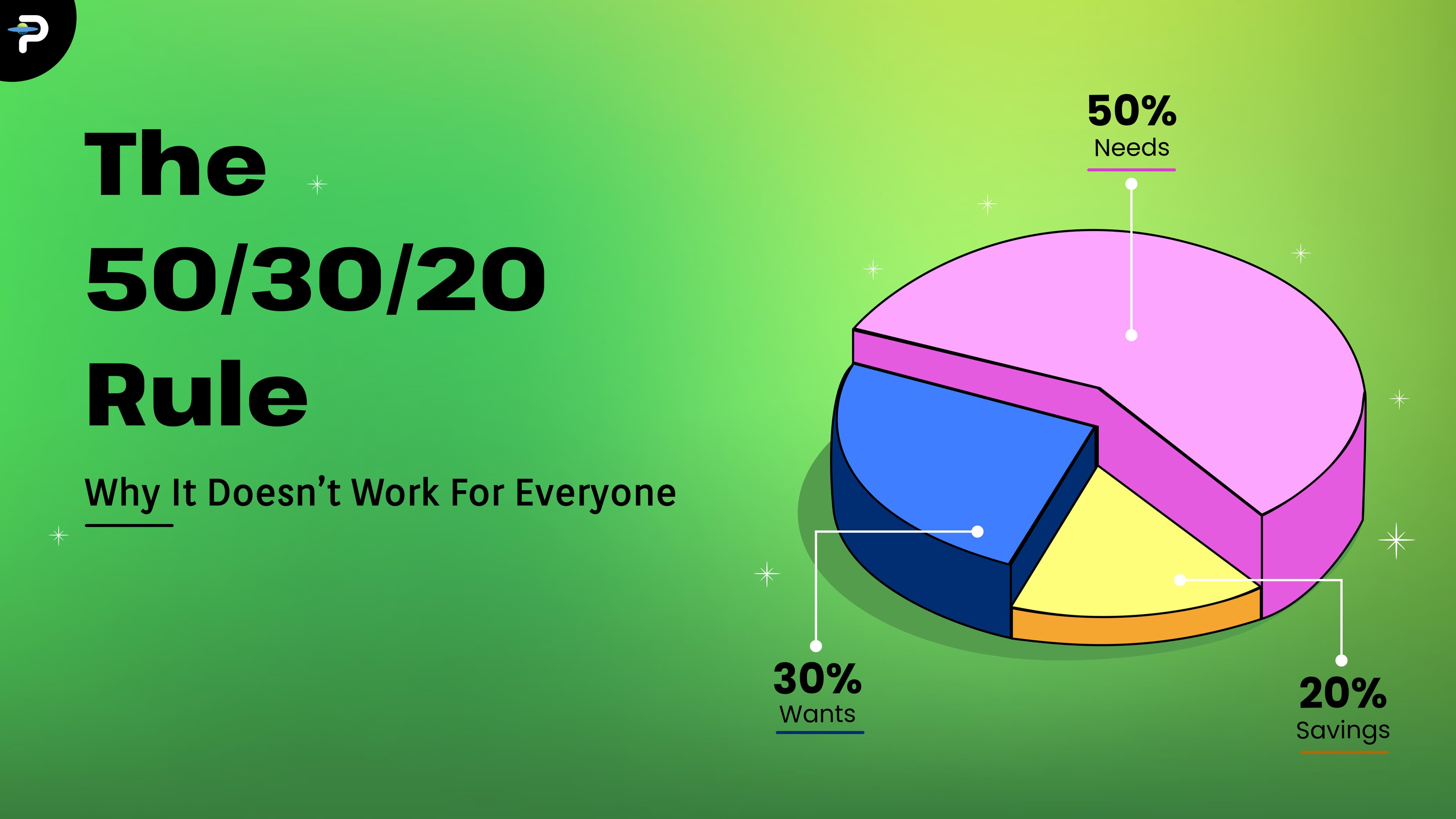

The 50/30/20 Rule and Why It Doesn’t Work for Everyone

Money advice is everywhere. You’ll see it on TikTok, in finance books, or from that one friend who swears they’ve “cracked the money code.” And one rule shows up again and again — the 50/30/20 rule. It says: spend 50% of your income on needs, 30% on wants, and save 20%.

We are a cutting-edge technology company specializing in software development, AI-driven solutions, and enterprise IT services. Founded in 2015, the company has established itself as a leader in digital transformation, helping businesses leverage technology for growth and efficiency.

4 months ago4 min read

0

Sounds neat, right? Balanced. Smart. Effortless. But real life doesn’t follow neat ratios. For most people today, this rule feels like a promise that never quite fits their reality. Let’s break down why.

The Rule, in Theory

The 50/30/20 rule became popular because of how simple it is. No complicated spreadsheets. No fancy jargon. Just three numbers.

So, if you make $4,000 a month, it says:

$2,000 for rent, groceries, and other “needs.”

$1,200 for fun stuff — travel, Netflix, maybe a dinner out.

$800 for savings or paying off debt.

The idea is to keep you balanced and responsible, but not deprived. In theory, it’s a great starting point. In reality, though, those numbers fall apart fast once you factor in the cost of actually living.

1. The Cost of Living Has Outgrown the Math

Let’s be honest. $2,000 doesn’t stretch very far anymore. In cities like New York, Los Angeles, or even Austin, rent alone can swallow $1,600. Add groceries, a phone bill, gas, and health insurance, and your “needs” are already at 80%.

The 50/30/20 rule was created in a time when rent didn’t demand half your paycheck. Today, housing, education, and healthcare costs have exploded. The math hasn’t kept up.

It’s not that people are bad with money. The math just doesn’t match modern life.

2. Income Isn’t Equal

This rule assumes everyone can follow the same formula, but someone earning $2,500 a month and someone earning $12,000 simply can’t play by the same rules.

For lower earners, “saving 20%” might sound like a dream. Most of their paycheck goes toward basic needs. For higher earners, saving just 20% could actually hold them back from bigger long-term goals like investing or early retirement.

Related Articles

Discover more articles you may like.

Sponsored Articles

Related Articles

Discover more articles you may like.

Top Writers

Some top of the line writers.

Best from Author

Best Articles from Top Authors

Top Writers

Some top of the line writers.

Best from Author

Best Articles from Top Authors

Money advice should scale with your income, not ignore it.

3. Family and Cultural Responsibilities Matter

In many families, especially outside the Western world — money isn’t personal. It’s shared. Maybe you help pay your parents’ bills, send money home, or cover your sibling’s tuition.

Try fitting that into a clean 50/30/20 split. You can’t. And you shouldn’t feel guilty for that.

A good budget respects your values and culture. It shouldn’t make you feel like you’re “doing it wrong” just because your priorities include family.

4. Debt Changes Everything

Student loans. Credit cards. Car payments. Medical bills. For many people, debt eats up a chunk of income long before they can even think about savings.

If 30% of your paycheck goes toward debt, you’re already breaking the “rule.” But that’s not failure, that’s just life.

The smart move is to focus on getting rid of high-interest debt first, even if it means saving less for a few months. A strict formula won’t tell you that, but your situation will.

5. “Wants” Aren’t Always Luxuries

Here’s where the 50/30/20 rule starts to feel out of touch. It puts things like Netflix, gym memberships, or mental health therapy into the “wants” category — as if they’re optional.

But in reality, those things often keep us grounded and balanced. A yoga class might be what keeps someone from burnout. Streaming shows might be their way of unwinding after long workdays.

Money isn’t just math. It’s emotional. A healthy budget allows for joy, not just survival.

6. Life Isn’t Static

A 25-year-old living alone and a 45-year-old with two kids won’t have the same financial rhythm. And that’s okay.

Maybe one month your car breaks down. Maybe your rent increases. Maybe you get laid off. A fixed ratio doesn’t bend when life does, and that’s why many people feel like they’re failing when they can’t stick to it.

A flexible budget that changes with your life is far more sustainable than a rigid one.

7. Inflation and Unstable Income Are the New Normal

Even if you’re earning the same salary, your money isn’t worth what it used to be. Inflation quietly eats into your budget, and those old percentages start to crumble.

For freelancers or gig workers, it’s even trickier. One month might be great, the next painfully slow. Trying to stick to fixed percentages when your income isn’t fixed can drive you crazy.

Instead of saying “I’ll save 20%,” try something like “I’ll save $400 this month if work is good.” That feels more human and more doable.

So, What Actually Works?

There’s no universal formula that fits everyone, but there is a way to make your money feel more under control.

Track where it goes. For one month, just watch your spending without judging it. You might be surprised where your money leaks.

Prioritize the essentials. Cover your needs first, then see what’s left.

Save what you can, not what you “should.” Even $100 a month adds up over time.

Plan for happiness, too. Budget for small joys without guilt, they keep you sane.

Review often. Your budget should grow and shift as your life does.

Budgeting is like exercise, it’s better to do something imperfectly than nothing at all.

The Bottom Line

The 50/30/20 rule isn’t bad. It’s just not built for everyone. It gives a sense of structure, but not the full picture.

Life today is unpredictable — rent spikes, side hustles, medical bills, family obligations. Trying to force your budget into a decades-old framework can feel like trying to squeeze into jeans that just don’t fit anymore.

Your goal shouldn’t be to hit perfect ratios. It should be to feel calm when you open your banking app.

Because real financial balance isn’t about math. It’s about peace of mind, knowing that your money is working for your life, not someone else’s formula.